- California Assembly OKs highest minimum wage in nation

- S. Korea unveils first graphic cigarette warnings

- US joins with South Korea, Japan in bid to deter North Korea

- LPGA golfer Chun In-gee finally back in action

- S. Korea won’t be top seed in final World Cup qualification round

- US men’s soccer misses 2nd straight Olympics

- US back on track in qualifying with 4-0 win over Guatemala

- High-intensity workout injuries spawn cottage industry

- CDC expands range of Zika mosquitoes into parts of Northeast

- Who knew? ‘The Walking Dead’ is helping families connect

Household debt seen as S. Korea’s $1 trillion potential time bomb

(Korea Times)

By Choi Kyong-ae

Soaring household debt, fueled by a series of government-led stimulus programs, is posing a greater threat to the nation’s economy, analysts said.

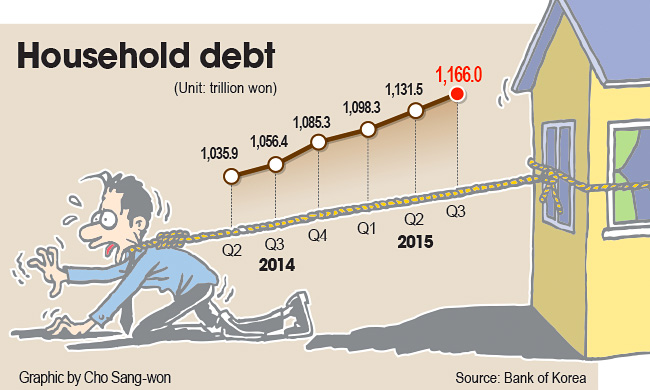

Household debt hit a fresh record of 1,166 trillion won ($1.01 trillion) at the end of September, jumping 10 percent from 1,056 trillion a year earlier, according to the Bank of Korea (BOK), Tuesday.

The debt, consisting of a combination of credit purchases and borrowings from financial firms, is at its highest level since the central bank began to compile data on it in 2002.

As the U.S. Federal Reserve in December is expected to raise its interest rate for the first time in almost a decade, analysts say that the debt may wreak havoc on the already weak economy.

Korea posted the highest household debt to GDP ratio of 84 percent among the world’s 18 emerging economies, including Hong Kong, Singapore and China, in the January to March quarter, according to a report from the Institute of International Finance (IIF).

“Household debt has skyrocketed over a short period of time propelled by the government’s deregulations that resulted in more borrowing at lower rates in the past year. It has now reached a level threatening the health of the national economy,” said Lee Sang-jae, an analyst at Eugene Investment & Securities.

While putting a brake on the rapid growth of household debt to GDP ratio, the Financial Services Commission (FSC) badly needs to ask banks to apply stricter rules when extending loans to customers and to restructure them to avoid massive non-performing loans, analysts said.

“Under the FSS’s guidelines, banks will have to change the terms for existing or future loans in order to allow customers to gradually pay back principal and interest to the lenders. This will help reduce possible bad loans in the case of financial volatility,” Lee said.

Currently, most customers are required to pay back interest only during a fixed five-year period or longer and then repay the principal in one go later.

To control the debt growth, the FSS introduced the loan conversion program this year which guides banks to convert to fixed rate, amortized loans from floating rate, or interest-only ones, with the Korea Housing Finance Corporation purchasing and securitizing the new loans from banks.

Foreign brokerages said that high household debt levels are likely already constraining spending ability, which they see in turn as weighing on the country’s GDP growth.

Rising household debt, often cited by the BOK as an argument against lowering the interest rate, remains a major structural impediment to Korea’s growth — projected by the central bank to be 2.7 percent — BNP Paribas economist Mark Walton wrote in a research note.

Citi Research economist Chang Jae-chul expressed concerns about the worsened quality of household debt.

“Among indebted households, those with debts from multiple financial institutions and less capable of repaying their debts have increased sharply on record-low interest rates,” he said.

Korea has held its key interest rate at an all-time low of 1.5 percent after four rate cuts since August last year in line with the government’s packages of stimulus measures which failed to buoy lackluster spending.

Korea’s household debt-GDP ratio was higher than the 74 percent average of advanced economies and more than doubled the 40 percent average among Asia’s emerging economies.

Related Posts

One Comment

-

U.S. dispels suspicion of little confidence in S. Korean intel over N.K. troop dispatch to Russia

U.S. dispels suspicion of little confidence in S. Korean intel over N.K. troop dispatch to RussiaA State Department spokesperson on Tuesday rejected the notion...

- October 23, 2024

ENTERTAINMENT

-

‘Amazon Bullseye,’ an overly familiar comedy

‘Amazon Bullseye,’ an overly familiar comedy“Amazon Bullseye” is a comedy that tries to blend...

- October 23, 2024

-

Age can’t stop Cho Yong-pil: K-pop legend’s triumphant return with 20th LP

Age can’t stop Cho Yong-pil: K-pop legend’s triumphant return with 20th LPSouth Korean music legend Cho Yong-pil proves that age...

- October 23, 2024

Pingback: Debts Go Credit Report | information - identity theft cases